[ad_1]

The most vital part of an automobile-loan is arguably the curiosity amount. It directly influences the dimensions of regular payments and in general loan tenor. Desire prices can even perform a job in the closing buying choice, impressive more than enough to override sentimental acquire explanations this kind of as model loyalty. It goes without the need of declaring, hence, that possible auto buyers spend interest to variables that ascertain their fascination rates when procuring for vehicle-financing solutions.

Just one of these kinds of components is the credit score. It is basically a weighted score that tells vehicle-loan providers how a great deal risk they are getting on by dealing with a possible borrower. You most probable have a credit score report if you have any credit rating accounts, such as credit playing cards, home loans or financial loans. This report then types the basis for deciding your credit score score.

It is not an actual evaluate, but it does drop gentle on things these as the borrower’s willingness and capacity to assistance the loan. Basically place, the greater your credit rating, the greater your possibilities of securing an automobile financial loan with favourable curiosity rates. This is significantly vital currently as we navigate the era of fascination fee hikes and inflationary pressures.

Utilizing your credit rating score to protected the very best interest costs

Through Experian

The all round purpose of the credit score score is common. However, different lenders in different components of the earth have their possess conditions to evaluate an individual’s creditworthiness. When you use for an car personal loan in the US, the loan company will operate a credit verify as component of the approach. The greater part of the lending institutions use FICO credit score scores. This is a 3-digit rating assigned to a borrower immediately after the credit check exercising.

It was initially formulated in 1989 by a facts analytics business called Reasonable Isaac Enterprise. These days, there are several variants of the FICO algorithm (and other scoring styles, for that issue), but they are all aimed at ascertaining the borrower’s skill to take on credit score.

By using The Stability

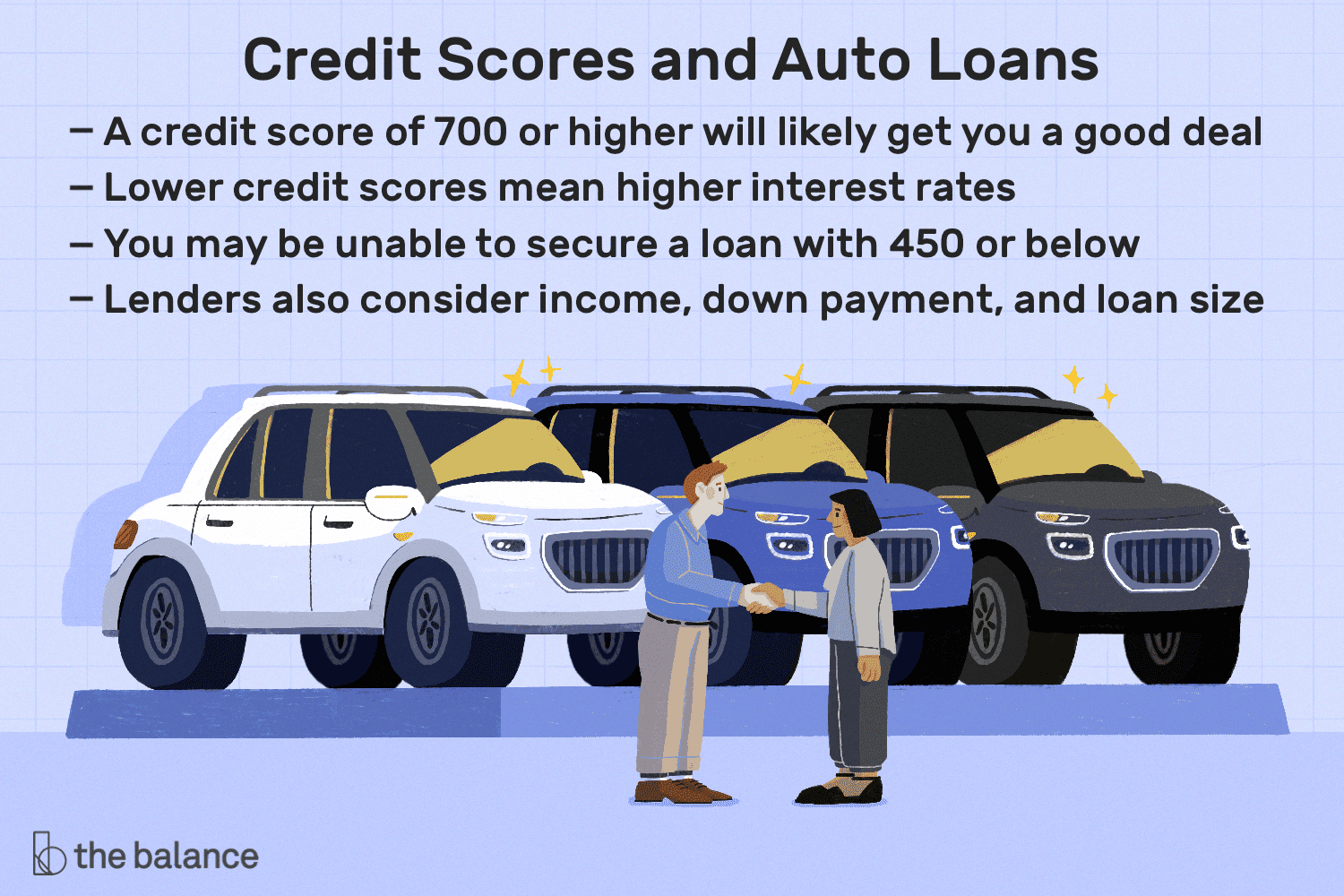

In accordance to the CFPB (Consumer Financial Security Bureau) Consumer Credit score Panel, there are 5 unique borrower profiles sorted into the subsequent credit rating buckets: Tremendous-primary (720 & previously mentioned) Primary (660-719) Near-key (620-659) Subprime (580-619) Deep subprime (underneath 580). A borrower with a score underneath 660 can however protected auto loans, but they will be much more expensive than a Prime or Super-prime borrower with a score north of 661. The logic listed here is that you will want to hold your credit score as substantial as achievable to get the most effective specials when buying for automobile financial loans.

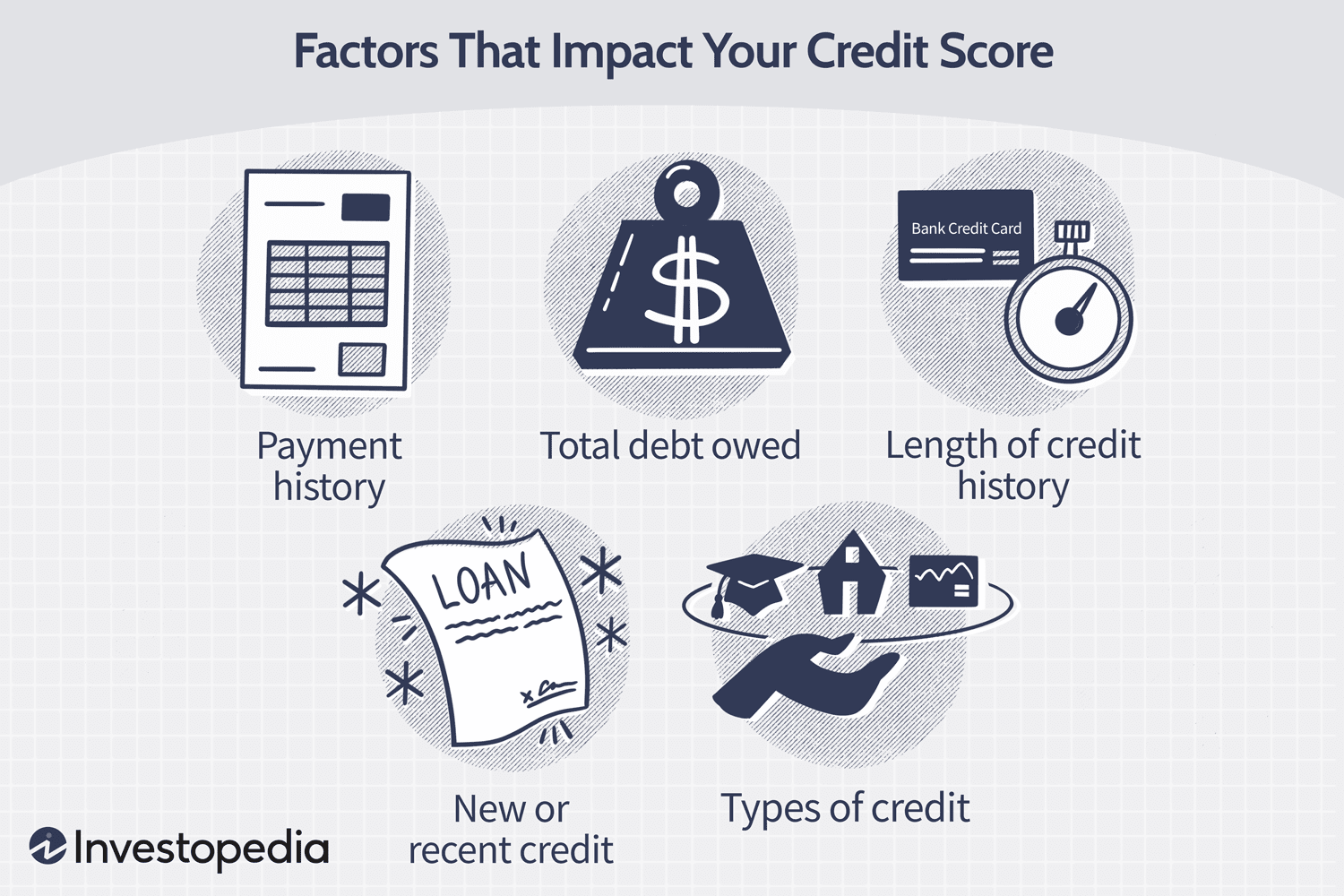

Things that damage your credit history rating

By means of Investopedia

An fantastic credit rating rating is the consequence of cautious and deliberate arranging, and recognizing the prospective pitfalls can help the borrower stay clear of producing missteps that pull down the rating into undesirable territory.

Producing a late payment

Payment historical past on your credit obligations accounts for up to 35% of the FICO rating. In accordance to FICO, a payment that is 30 times late can charge a person with a credit rating rating of 780 or better anywhere from 90 to 110 factors. It is vital to make payments as at when due and proactively attain out to the financial institution if, for any cause, payment will be delayed.

A high financial debt-to-credit history utilization ratio

Credit score background is constructed by a continuous cycle of credit utilization and spend downs. However, you will want to retain an eye on the proportion of your debt load to total credit rating. The lower your balances relative to your complete obtainable credit rating, the greater your rating will be.

Non-utilization of credit

On the other hand, no credit history record for an prolonged interval can also adversely influence the borrower’s credit score score. Loan providers and collectors have practically nothing to report to credit rating bureaus when you really do not utilize your credit score accounts. This will make it much more tough to appraise upcoming bank loan applications.

Bankruptcy

Filing for personal bankruptcy has one particular of the most substantial impacts on your credit score score. It can wipe as considerably as 240 points from an individual’s score, and what’s much more? A bankruptcy report can remain on the credit history heritage for up to ten many years.

This listing is by no suggests exhaustive, and other factors such as frequency of credit history purposes, credit history card closure, charge-offs and refinancing all affect credit history scores in different degrees.

Bettering your credit score rating

Improving your credit score score will entail preventing the pitfalls before recognized higher than. Methods this kind of as prompt and standard monthly bill payments, sustaining a small personal debt-to-credit history utilization ratio (ideally about 30%), trying to keep credit score card accounts open up and preventing many personal loan applications at when are all actions in the appropriate path.

Nevertheless, even with all these ‘building blocks’ in location, a great credit rating score is not instantaneous. It might choose a even though to see any improvement, especially because unfavorable experiences can keep on your credit rating heritage for various years. There is no rigid time body for credit score rating development as every single person’s monetary condition is exclusive. According to Forbes, it could get any place from a month to as significantly as 10 a long time. Obviously, this is affected by elements such as the individual’s recent credit score position and amount of money of total exposure.

Securing vehicle loans no matter of credit rating score

By way of Geotab

A high credit rating score will undoubtedly strengthen your possibilities of securing auto financing and locking up the most effective fascination costs. On the other hand, it is not all doom-and-gloom for prospective car or truck potential buyers with weak scores as they are not fully devoid of choices.

No matter of your credit rating score, looking close to and looking at the many financing alternatives is highly proposed. It is just like purchasing for the vehicle by itself an typical purchaser will assess diverse dealerships and negotiate vigorously ahead of building the last selection.

Financial institutions are the conventional sources for getting a mortgage, but you may be proscribing your possibilities if they are your only thought. Never overlook substitute loan companies. Operating with 3rd-celebration financing providers, these types of as finding your automobile financial loan via LoanCenter.com, may well deliver you with favourable fascination costs or funding phrases.

It is vital to note that just obtaining vehicle-mortgage preapprovals (various from true personal loan purposes) while browsing close to will not effect your credit rating score considering that most scoring products do not take care of this as a challenging enquiry.

In summary, a weak credit score may well push the lowest fascination costs out of achieve. However, getting quite a few alternatives will strengthen your odds of locating a bundle with an desire price that suits within your spending plan and enable you to obtain your wanted car.

[ad_2]

Source website link